Inquiries Effect on Credit Scoring

Many people have heard before that inquiries lower the score. As a result many customers will ask you whether this is true or just a myth. Inquiries definitely impact the consumer credit score.

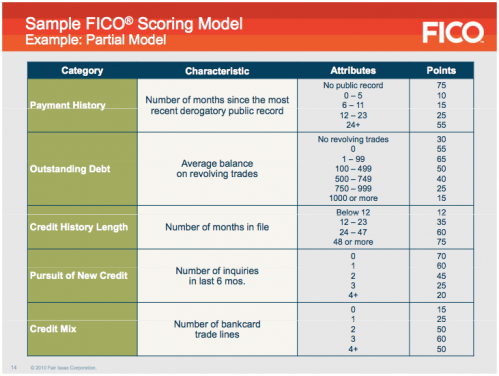

FICO score inquiries account for 10% of the total credit score. FICO counts this to the part of their score that deals with the accumulation of new debt.

If consumers apply for a lot of credit within a short period of time, their scores will go down. There is no set amount of drop per inquiry - it's bundles of inquiries in a short period of time that really impact the score, not just one single inquiry.

This means that when a customer applies for something and an inquiry is put on their report, their score might not go down at all. But if they start applying for a lot of new credit in a short period of time, these groupings of inquiries will have an impact on their score.

However, there are exceptions: mortgage or auto loans. If they go to apply for a mortgage, all mortgage inquiries within a 2 week time period only count as 1 inquiry on their credit report. The same applies for auto loan inquiries.

The reason for this, is that the score providers understand that consumers will commonly shop around for the best terms on home and auto loans, and they shouldn’t be punished for doing this. Plus, in the auto business, it is common for the consumer’s application to be sent to many different banks, which could also lower their scores, if FICO didn’t operate this way.

Accumulation of new credit or new inquiries on the report, accounts for 10% of the total credit score, Insure your clients know about this, so they can minimize the amount of inquiries they put on their report further maximizing their scores.

For more details about your credit score and to learn ways to improve your credit status, please contact a representative at Precision Credit Restoration at 877-292-0656. We are here to guide you from financial distress to financial success.

FICO score inquiries account for 10% of the total credit score. FICO counts this to the part of their score that deals with the accumulation of new debt.

If consumers apply for a lot of credit within a short period of time, their scores will go down. There is no set amount of drop per inquiry - it's bundles of inquiries in a short period of time that really impact the score, not just one single inquiry.

This means that when a customer applies for something and an inquiry is put on their report, their score might not go down at all. But if they start applying for a lot of new credit in a short period of time, these groupings of inquiries will have an impact on their score.

However, there are exceptions: mortgage or auto loans. If they go to apply for a mortgage, all mortgage inquiries within a 2 week time period only count as 1 inquiry on their credit report. The same applies for auto loan inquiries.

The reason for this, is that the score providers understand that consumers will commonly shop around for the best terms on home and auto loans, and they shouldn’t be punished for doing this. Plus, in the auto business, it is common for the consumer’s application to be sent to many different banks, which could also lower their scores, if FICO didn’t operate this way.

Accumulation of new credit or new inquiries on the report, accounts for 10% of the total credit score, Insure your clients know about this, so they can minimize the amount of inquiries they put on their report further maximizing their scores.

For more details about your credit score and to learn ways to improve your credit status, please contact a representative at Precision Credit Restoration at 877-292-0656. We are here to guide you from financial distress to financial success.