Few credit related topics confound, confuse, and befuddle consumers like the subject of credit scores.

Popular television commercials, misinformed advice columnists and pretend credit experts are notorious for suggesting that consumers have only one credit score. Nothing could be further from the truth. The reality is consumers don’t have just one credit score but hundreds of different credit scores.

Equifax, Trans Union, and Experian are the three major credit bureaus that are responsible for maintaining data on more than 600 millions U.S. consumers about their credit management habits. The credit bureaus compile this data into credit reports and sell the information to lenders, insurance companies and even to consumers.

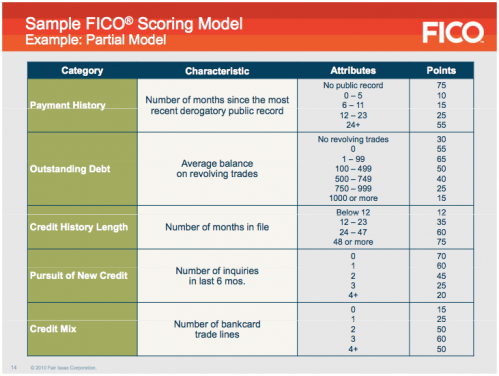

Credit scoring models are used to interpret and analyze the data on the credit reports housed by the credit bureaus. VantageScore and FICO are the two companies that produce credit scoring software used to calculate the most common credit scores. The credit scoring models designed by these two companies are similar, but they are certainly not identical and will certainly generate different credit scores for any given consumer.

At least 70 credit scores

To add to the confusion, there are different software versions for every credit scoring model that is commercially available. Under the FICO brand/umbrella there are about to be somewhere around 65 different scores available for purchase and use by lenders. Under the VantageScore brand there are nine.

Counting just the credit bureau based credit scoring systems there are well over 70 different scoring models, which means you’ve got at least 70 different scores.

In addition to the credit bureau based scores like FICO and VantageScore there are countless other credit scores being used by lenders and insurance companies. Most of these companies will use custom developed scoring models that consider both credit report and non-credit report data, like information from an application.

These “custom application scores” are actually much more common than FICO and VantageScore credit scores. Most large lenders have several of these models in use at any given time.

Consumers almost always neglect the large number of non-risk scores that are being sold by the credit bureaus to lenders.

These marketing scores often measure the likelihood that you’ll respond to a credit card offer, leave for a competing lender, and generate a positive revenue flow. While these scores are not as commonly used as risk scores, they are still fairly common.Keeping track of the hundreds of credit scoring possibilities would be exhausting and is nearly impossible. Most of these scores aren’t even available for consumers to obtain under any circumstance.

Keeping track of so many scores

Keeping track of the hundreds of credit scoring possibilities would be exhausting and is nearly impossible. Most of these scores aren’t even available for consumers to obtain under any circumstance.

Having said that, there is still an effective way for consumers to control their credit scores. Credit scores are based on the data contained in a consumer’s credit reports, nothing more and nothing less. By controlling the information contained on your credit reports you can effectively take charge of your credit scores.

If you pay your bills on time and maintain modest amounts of debt then you’re going to have a good score regardless of the brand or the model. If you miss payments or get into too much credit card debt then you’re going to have poor credit scores.

The bottom line is that it’s much easier to manage the data on three credit reports than it is to chase around hundreds of credit scores.

For more information regarding your credit status, please feel free to reach out to the credit experts at Precision Credit Restoration at 877-292-0656. Let us guide you from financial distress to financial success.

For more information regarding your credit status, please feel free to reach out to the credit experts at Precision Credit Restoration at 877-292-0656. Let us guide you from financial distress to financial success.

No comments:

Post a Comment